Ear to the ground

14 March 2025

Uncertainty continued to embroil markets this week. The US continues to place tariffs on specific goods from particular nations, which is typically met with a counter tariff of their own. We know that this has not yet reached its conclusion, with the beginning of April bringing insight to the size and scope of reciprocal tariffs which Trump has promised will be imposed on its trading partners. We aren’t yet in a position of an outright global trade war but there is certainly enough rhetoric to keep markets uncertain.

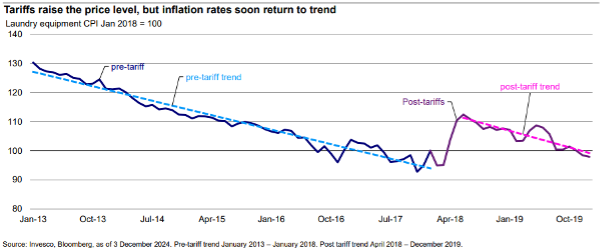

The concern continues to cause unease in both equity and bond markets. In the latter the immediate fear is of course inflation. Tariffs mean that imported goods cost more. Whilst the desired effect is that home produced goods become more attractive to the end user, it would perhaps be false to believe that local producers won’t take the opportunity to hike their prices also. Even if it were to a pricing point just below that of the imported goods, it is inflation all the same. A short term pick up is therefore not out of the question, however history has shown that it can prove to be short lived.

At the same time the outlook for economic growth does not look as healthy as a consequence. This has coincided with a fall in US expectations as covered in last week’s edition, and has resulted in weakness in the US equity market. The Russell 2000 index, which enjoyed such strong gains following Trump’s inauguration, has now given up all those gains and then some. From the 19th February to the 13th March close, the index is down over 12.5%, meaning it has entered correction territory. Weakness has also been seen in the tech heavy Nasdaq Composite index, where perhaps valuations were considered to be a little frothy, shall we say. Over the same period it is down over 13.5% and therefore also in a state of correction. The dominance in terms of weighting of the Magnificent 7 stocks within the S&P 500 index also means that it flirts with correction territory.

It is perhaps too early to call whether this is the initial turn of an inflection point, in terms of global stock excluding US having their time in the sun. Or perhaps if this period has been one whereby we are simply seeing some exuberance being removed from the market. Only time will tell.

Such has been the noise around tariffs that economic data almost took a back seat this week. In the US we did see the release of the latest inflation figures. Here there was some good news for the US Federal Reserve, at least for now, with it falling to 2.8% year on year to February. Not only was this below the previous reading of 3% but also the consensus forecast of 2.9%. The central bank prefer to focus on the core rate and here there was also good news, coming in at 3.1% year on year, down from 3.3%, so at least it is moving in the right direction.

In the UK January’s economic growth was a little behind expectations, the economy actually shrinking in the month by -0.1%, compared to an expected expansion of 0.1%. Year on year growth was therefore slightly weaker than expected at 1%. Despite these figures the equity market is in positive territory on Friday, climbing over 1%. No doubt a response to a rebound in US markets, but these figures also perhaps raise the prospect for further interest rate cuts by the Bank of England.

This article is for information purposes only and should not be construed as advice. We strongly suggest you seek independent financial advice prior to taking any course of action.

The value of this investment can fall as well as rise and investors may get back less than they originally invested. Past performance is not necessarily a guide to future performance.

The Fund is suitable for investors who are seeking to achieve long term capital growth.

The tax treatment of investments depends on the individual circumstances of each client and may be subject to change in the future. The above is in relation to a UK domiciled investor only and would be different for those domiciled outside the UK. We strongly suggest you seek independent tax advice prior to taking any course of action.

Subscribe Today

To receive exclusive fund notifications straight into your inbox, please complete this form.